Our website is using cookies to deliver best possible experience to you. By using it you agree to cookies policy.

The Digital Poland Foundation has published the fifth edition of the Digital Champions CEE 2026 report, which presents the 100 most valuable technology companies in Central and Eastern Europe. The combined value of the digital champions in the ranking reached USD 127.9 billion. However, the data paints a picture of a market which, on the one hand, is growing thanks to deep tech innovations, whilst on the other, is grappling with a wave of relocations of the largest companies outside the region.

Steady growth and untapped potential

At the end of 2025, the combined market capitalisation of the 100 largest technology companies in the CEE region reached USD 127.9 billion, representing a year-on-year increase of 9.36%. This result is slowly bringing the ecosystem closer to the record valuations of 2021 and confirms the enduring resilience of the regional digital economy. The biggest drivers of growth were the so-called digital phoenixes – companies valued at over $1 billion. Their combined valuation grew by 14.58% year-on-year, reaching $101.05 billion.

However, official data significantly underestimates the actual scale of value being created in the region. Central and Eastern Europe is home to powerhouses such as Avast, Grammarly, ElevenLabs, Preply, People.ai and Rimac. Many of them have moved their headquarters abroad to raise capital more efficiently, or have been acquired by foreign corporations. According to the report’s authors, had these companies remained in our region and continued to qualify for the ranking, the total value of the top 100 companies would now exceed USD 170 billion.

“When the inaugural Digital Champions CEE ranking was launched, the region was framed as a ‘Digital Phoenix’ — a symbol of ambitious transformation emerging from post-communist economies. Five editions later, the trajectory remains strong, but the narrative has evolved.

Against a backdrop of intensified global headwinds, companies across Central and Eastern Europe have shifted from rapid acceleration to more disciplined, resilient growth. This maturation has sharpened strategic focus: for many organisations, it has unlocked new avenues for expansion and innovation; for others, it has introduced heightened competitive pressure and a more complex, unpredictable operating environment,” said Radzym Wójcik, Counsel at Baker McKenzie.

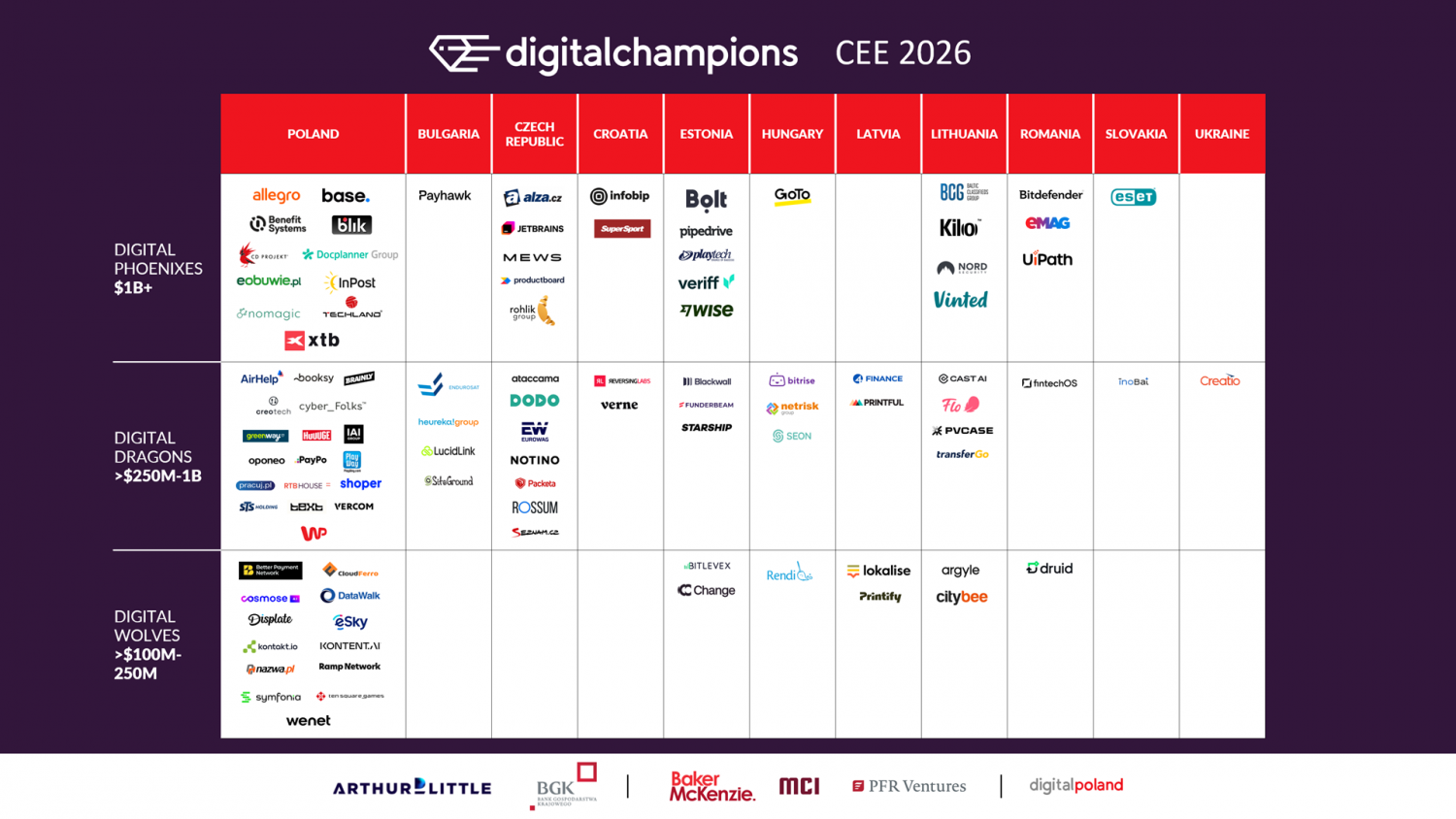

Poland leads in size, the Baltic states lead in market penetration

Poland remains the market with the highest total company value in this part of Europe. The top 100 list includes as many as 42 Polish companies (the highest number in the entire region), which account for USD 47.39 billion, or 37.05% of the total value of the ranking. In turn, our country is the only market in the region with such a strong presence of companies at every stage of development, from young scale-ups to billion-dollar corporations.

However, if we look at the density of companies per 100,000 inhabitants, the Baltic states remain the clear leaders. Estonia achieved the highest score in the region. Lithuania is also growing extremely strongly, having increased the total value of its tech companies by as much as 123.97% since 2021, whilst Latvia proved to be the fastest-growing country in terms of growth over the last five years. The top four in the ranking – Poland, Estonia, Lithuania and the Czech Republic – currently account for nearly 78% of the total value of companies in the list.

A shift in structure: time for deep tech and defence

E-commerce and marketplace platforms remain the most significant sector in the ranking, accounting for over 36% of its value. However, the report highlights a significant shift in focus – investors are increasingly looking towards deep tech, healthtech, space technology and security solutions. The most dynamic category turned out to be the “other” group, whose value rose by as much as 87.59% year-on-year. This includes, among others, deep tech and space tech companies. The ranking also features companies such as EnduroSat and Creotech Instruments, confirming the boom in technologies related to infrastructure, logistics and the strategic resilience of economies.

The situation in the cybersecurity sector is interesting: although the number of companies has risen by 20% since 2021, its total value has fallen due to the high-profile acquisition of Avast for USD 8.4 billion. This development is making way for a new generation of young defence companies, whose growth has been accelerated by the war in Ukraine.

“The composition of the ranking is also evolving. E-commerce, SaaS and fintech remain the backbone of CEE’s digital economy, but the list now points to a broader and more strategic technology base: robotics, space and Earth observation, cybersecurity, AI-native software, digital health, sovereign cloud and other infrastructure-oriented businesses. This shift shows that CEE is moving beyond consumer platforms and software scale-ups toward technologies directly linked to Europe’s productivity, security, resilience and digital sovereignty,” said Wojciech Świercz, Partner at Arthur D. Little.

The challenge of relocation – is Europe merely a research base?

The most serious structural problem identified in the report is the widespread tendency for successful companies to relocate their headquarters to Western markets. As many as 48% of scale-ups from the region have relocated their headquarters abroad in order to secure more growth capital. The United States is the leading destination for talent from Central Europe (56% of relocating companies), whilst within Europe itself, the UK leads the way.

This trend poses a serious threat to European competitiveness. As Piotr Mieczkowski, managing director of the Digital Poland foundation, warns, “ideas are conceived locally, products are built locally, but financing, scaling and often final acquisitions take place outside Europe”. This reduces our continent to the role of a highly skilled research and development base for the American technology market.

Maturity and a new generation of leaders

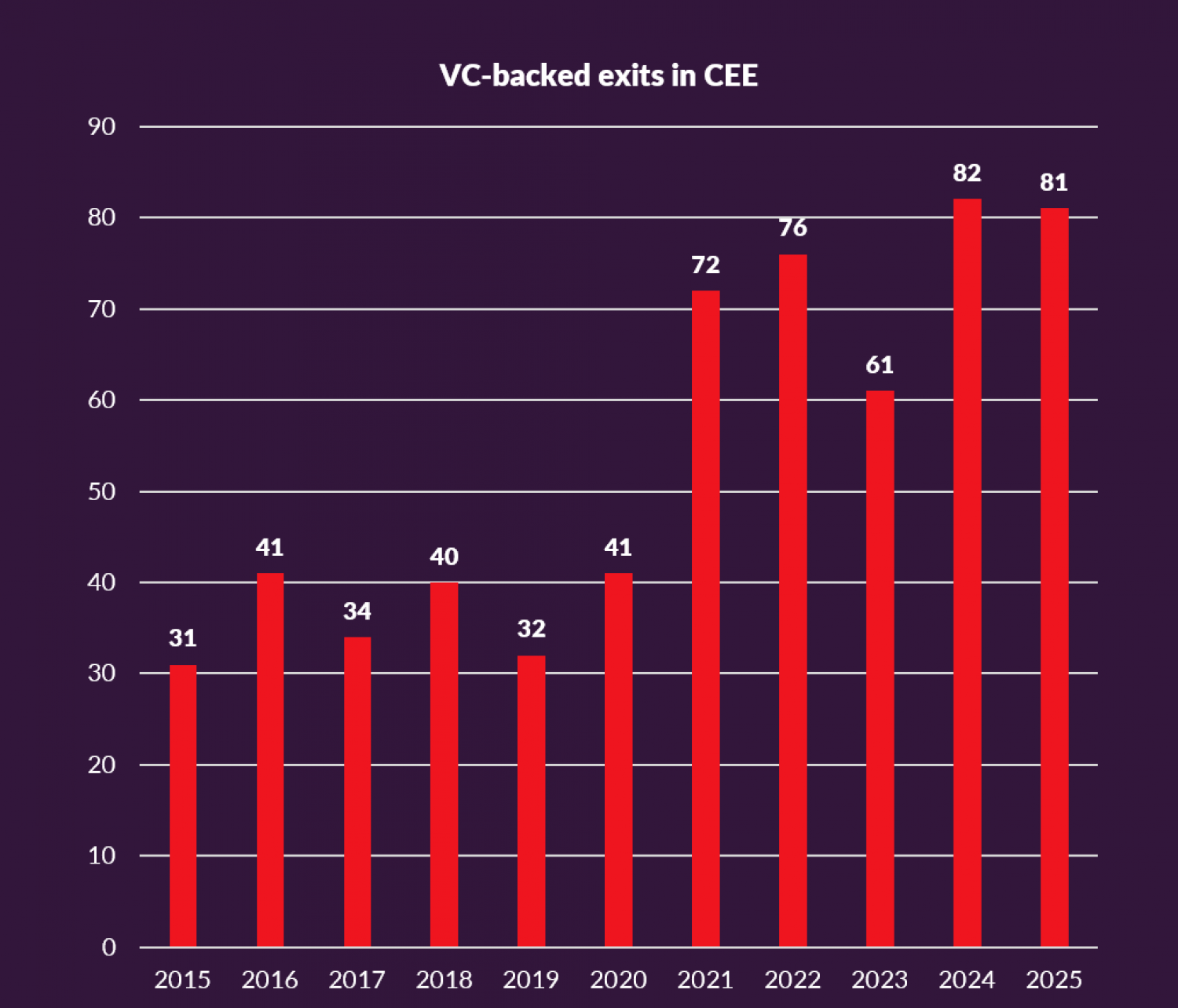

Despite the above challenges, the CEE market is performing very well in terms of investment and fund exits. Following a historic record of 82 exits in 2024, the market maintained a very high level, ending 2025 with 81 transactions. This proves that the CEE region is now capable of regularly creating companies ready for IPOs and acquisitions.

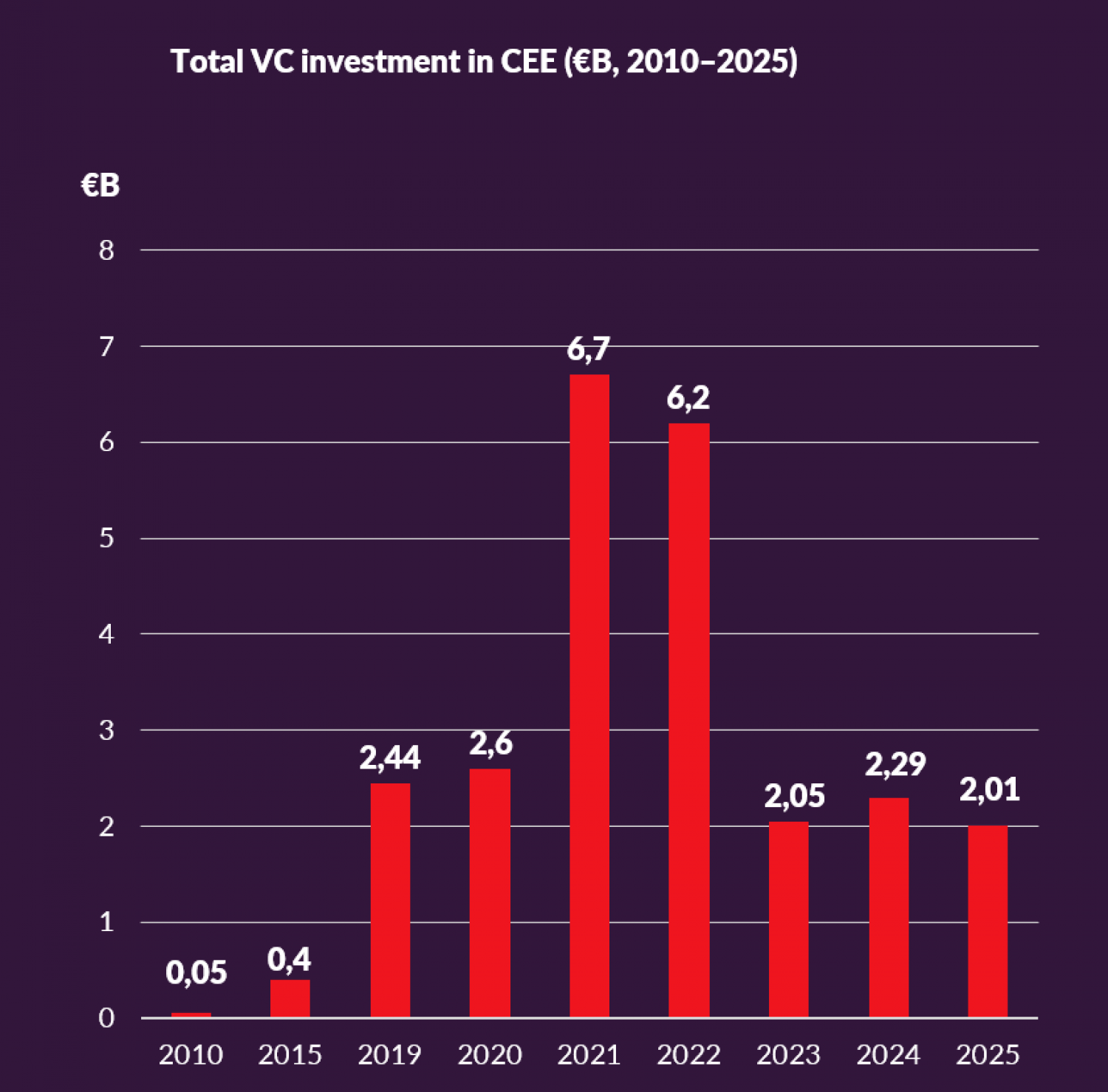

The total value of VC investment in 2025 stood at €2.71 billion (including €730 million in capital raised by companies that have already relocated from the region, such as ICEYE, ElevenLabs and Tachyum).

A generational shift is also evident. Since the first edition of the ranking, young companies established between 2017 and 2021 have stood out for their most dynamic growth (as much as 189.09%). At the same time, 49 companies have maintained their position in the top 100 of the ranking across all five editions of the report. This shows that, alongside new, rapidly growing firms, the region is also building an increasingly stable group of mature technology leaders.

“Innovation today is the foundation of competitiveness, resilience and technological sovereignty for Poland and Europe. This is why BGK actively engages in building the innovation financing ecosystem through the Innovate Poland initiative, including the Future Tech Poland fund, as well as through the BGK Vinci investment fund. We also invest directly in funds supporting modern technological infrastructure.

The Digital Champions CEE 2026 report demonstrates that our region possesses the talent, ambition and entrepreneurial strength which — with the right support — can translate into the growth of future European and global technology leaders,” said Jarosław Dąbrowski, Member of the Management Board at Bank Gospodarstwa Krajowego.

The Digital Champions CEE 2026 report, produced by the Digital Poland Foundation, can be downloaded free of charge from the foundation’s website. The strategic partners are Arthur D. Little and Bank Gospodarstwa Krajowego. Other partners include Baker McKenzie, MCI Capital and PFR Ventures.