Our website is using cookies to deliver best possible experience to you. By using it you agree to cookies policy.

We have had an exceptionally busy few days and witnessed one of the most important market events of the year. During the international “Capital for Growth” conference, organised in Warsaw by Bank Gospodarstwa Krajowego, our managing director, Piotr Mieczkowski, officially presented the findings of the fifth edition of the “Digital Champions CEE 2026” report

The event, which brought together managers from leading VC/PE funds, financial institutions and technology leaders, provided a double dose of strategic insight. Alongside our ranking, a key report by BGK analysts entitled “Capital investment in CEE: opportunities for local and global investors” was also launched there. Both documents address the same fundamental problem: how to bridge the massive capital gap and retain the most valuable innovations in our region.

A trillion euros in needs and a funding model that is reaching its limits

From the perspective of the Digital Poland Foundation, the debate on the region’s capital structure is crucial for the further development of innovation. The BGK report explicitly states that traditional funding models based on EU funds and public debt are now reaching their limits. Experts estimate the annual investment needs of the infrastructure sector alone in Central and Eastern Europe (CEE) at between 65 and 75 billion euros, to which must be added over 50 billion euros annually for the maintenance of existing networks. In the longer term, this translates into a total investment gap of around €1 trillion, which could take between 10 and 20 years to close. Against the backdrop of a projected decline in the inflow of EU funds, mobilising long-term private capital is becoming crucial.

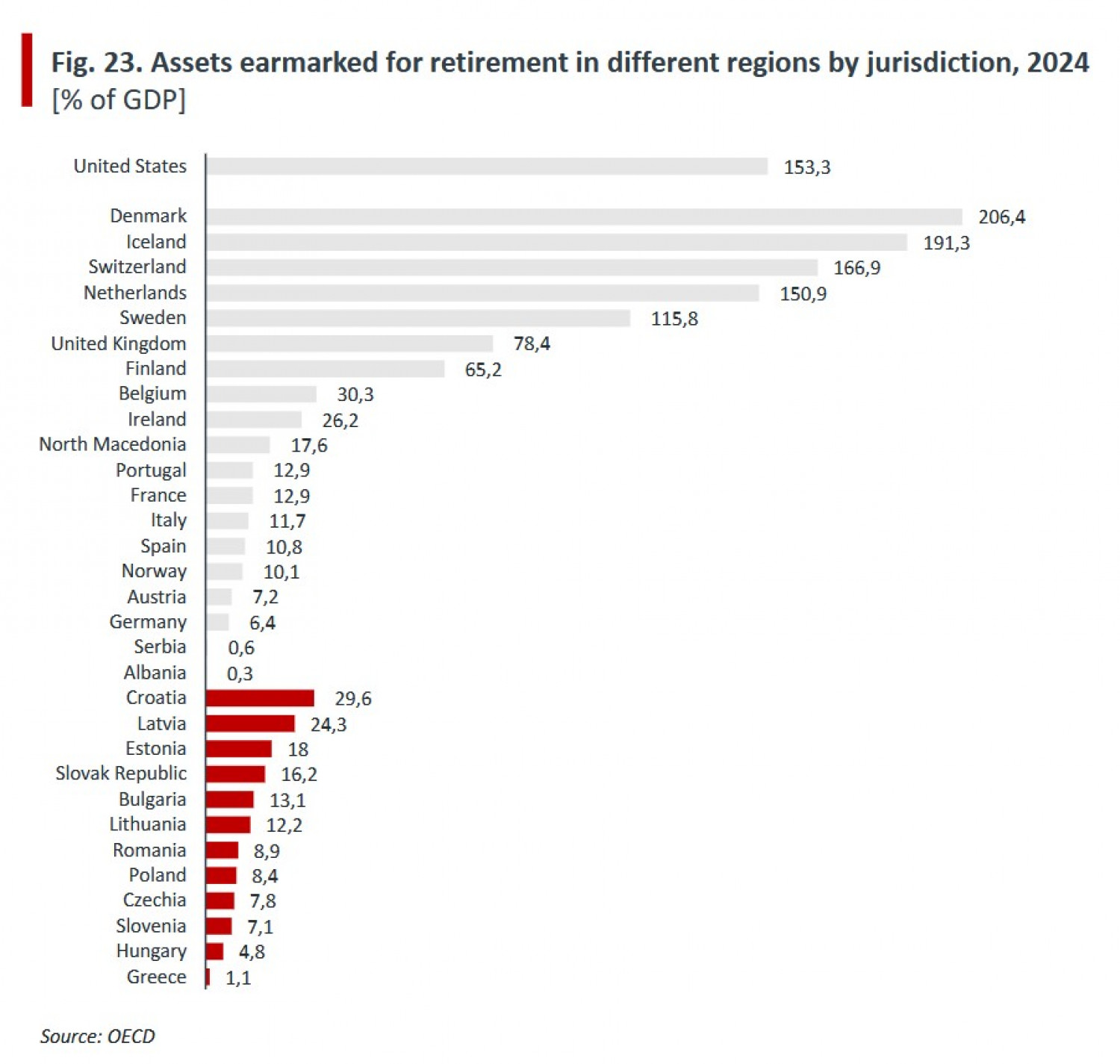

Currently, the private equity market in CEE countries shows a strong reliance on sources that are not easily scalable. Banks play a dominant role, accounting for 26 per cent of capital, alongside government agencies, which account for 20 per cent. However, such a system does not create a stable, self-sustaining investment cycle, as these institutions rarely provide capital with a profile suitable for high-risk VC/PE or long-term mega-projects. The main barrier remains the architecture of pension systems. Whilst in Denmark the assets of capital pension funds exceed 200 per cent of GDP, in CEE countries this figure stands at only around 10 per cent of GDP. Shallow stock markets (market capitalisation in CEE is only 17 per cent of GDP in 2024, compared with 170 per cent in Sweden) further cut companies off from capital at later stages of development.

Digital champions are growing, but are leaving the region in search of capital

This underfunding is clearly evident in the results of our latest ranking of the 100 most valuable technology companies. The combined market capitalisation of the 100 digital champions from Central and Eastern Europe reached USD 127.9 billion by the end of 2025, marking a year-on-year increase of 9.36 per cent. The strongest growth was seen among the largest players – the so-called ‘digital phoenixes’ valued at over US$1 billion. Poland remains the undisputed leader of the ranking, accounting for US$47.39 billion of the total value and placing as many as 42 companies in the top 100.

However, these optimistic figures mask an extremely worrying trend, which we as the Foundation strongly condemn. As many as 48 per cent of regional scale-ups have already moved their headquarters abroad, mainly to the United States and the United Kingdom. Companies are doing this for one reason — they are seeking greater growth capital, which they cannot find in their domestic markets, which are too shallow. If the companies that have left the region or been acquired since 2021 (such as ElevenLabs) still met the ranking criteria, the combined value of the top 100 companies would today exceed US$170 billion. In this way, Europe is increasingly being reduced to the role of a highly skilled research and development base for the US tech sector. We develop ideas and products locally, but it is investors from other continents who reap the rewards in the form of scaling and exit deals.

A new wave of innovation

Together with our partners, we have also observed a clear structural shift in the CEE ecosystem. Whilst e-commerce and marketplace platforms still account for over 36 per cent of the ranking’s value, a new generation of leaders is coming to the fore. The fastest-growing category turned out to be the group comprising deep tech, space tech, healthtech and solutions developed for national security purposes. The value of this group rose by as much as 87.59 per cent year-on-year, and new, strong players such as Creotech Instruments have appeared in the ranking. The war in Ukraine has undoubtedly accelerated the development of defence technologies and cybersecurity. The region is clearly moving beyond the model of simple consumer platforms, heading towards innovations that build Europe’s digital sovereignty.

Despite structural problems with the supply of domestic capital, CEE markets offer investors something unique – they exhibit higher return on sales and return on assets ratios than the core of the eurozone. This shows that Central and Eastern Europe remains an undervalued region which, at the same time, delivers above-average returns on investment. However, if we are to build global tech leaders and finance modern infrastructure, we must jointly implement regulations that mobilise long-term private savings and engage pension funds more closely. As the Digital Poland Foundation, we will consistently support these changes.

The Digital Champions CEE 2026 report is now available to download free of charge from the ‘Publications’ section of our website. We would like to extend our sincere thanks to the strategic partners of this edition: Arthur D. Little and Bank Gospodarstwa Krajowego, as well as the partners of this year’s edition: Baker McKenzie, MCI Capital and PFR Ventures.